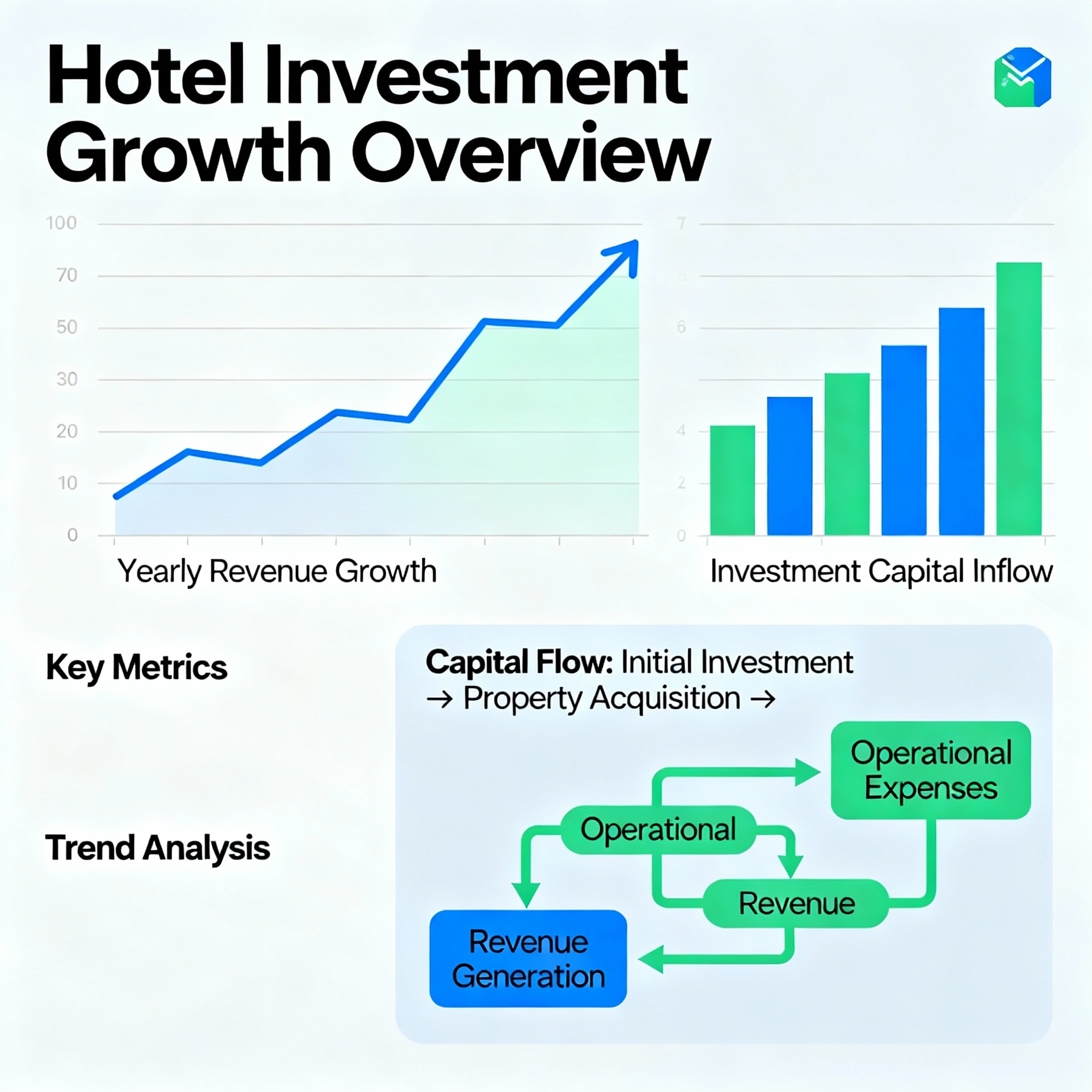

After two quieter years, Europe’s hotel market moved decisively back onto investor agendas. 2024 transactions jumped to €17.4bn (+62% YoY), the strongest since 2019, and H1-2025 kept momentum with ~€10.4bn, above the decade average. Single-asset deals led activity, while average keys per asset increased and pricing recalibrated modestly.

Performance drivers remained tangible, not speculative: ADR did the heavy lifting while occupancy stabilized at high levels; 2025 RevPAR growth for Europe is projected in the ~1.7% range (downgraded but still positive), with urban markets outpacing suburban.

Bottom line: capital is rotating into hotels because NOI growth is manufacturable—via brand/operator conversion, targeted CapEx, channel discipline, and product mix—at a time when other asset classes still face repricing and structural uncertainty.

What actually changed: the investment case in 2024–2025

- Deal volumes recovered. Europe’s hotel transaction market surged in 2024 and sustained a high run-rate into H1-2025, signaling renewed underwriting confidence and improved bid-ask alignment.

- Operating metrics are durable. Even with uneven monthly prints, the direction of travel for RevPAR in 2025 is positive; ADR remains the main lever, and urban nodes lead the growth stack.

- Global capital prepared to deploy. Major houses expect investment volumes to exceed 2024 by ~15–25% given maturities, deferred CapEx, and PE fund cycles—unlocking sales processes.

- Tourism fundamentals are intact. EMEA outlooks continue to call for steady travel demand supporting RevPAR through 2025.

Where the money is going (and why)

- Urban upper-midscale/upscale

These assets benefit from corporate travel normalization and event calendars. Investors like the control knobs: distribution, pricing governance, and brand conversion that can lift ADR without sacrificing occupancy. STR’s 2025 view: urban outperformance versus suburban. - Long-season resorts

Southern Europe’s coastal and island markets continue to monetize ADR via package design (wellness/medical-wellness, gastronomy, sports) and public-area refreshes that raise ancillary spend. While monthly RevPAR can be choppy, the annualized trend remains constructive. - Single-asset deals > portfolios

H1-2025 saw single-asset transactions at the forefront, with more keys per asset but slightly lower average price per room versus H1-2024—evidence of selective recalibration rather than a capitulation.

Pricing and returns: translating RevPAR into value

A typical European 4★ hotel with solid execution can still manufacture NOI:

- Illustrative base: ADR €130–150; occupancy 65–72% ⇒ RevPAR ~€85–€108.

- Operational plan: brand/collection conversion, room soft-CapEx (€8–12k/key), revenue governance, and mix enhancements.

- Realistic uplift: ADR +€10–€18 and +2–3 pts occupancy over 18–30 months (ranges observed across multiple markets in 2024–2025 reports). Assuming 35–45% flow-through on incremental revenue, NOI compounding becomes visible.

- Valuation math: at 11–13× NOI—consistent with mid-market European trades—each €1 of stabilized NOI adds €11–€13 of value, which is why committees focus on credible bridges, not just headline RevPAR.

- Investor takeaway: in 2025, equity stories that win are the ones that show exactly how ADR uplift and minor occupancy gains cascade to NOI—with believable operator/brand partners attached.

The NOI playbook investors want to see

- Brand/operator strategy that fits the box

Show why management vs franchise is chosen, and why this flag’s distribution and RM capabilities beat the status quo. Tie it to measurable ADR lift and direct-mix gains. (Institutional interest here remains strong across 2024–2025 outlooks.)

JLL - Targeted CapEx, not cosmetic

Bathrooms, lighting, HVAC, and key public areas yield the quickest ADR response; “museum” spaces convert into revenue (banquet/event/rooftop). Investors want phased CapEx tied to seasonality and a clear payback path referenced to comp sets.

Cushman & Wakefield - Channel and pricing discipline

Replace blanket OTA discounting with a structured rate fence and packaging. The goal isn’t 2 more points of occupancy at any cost—it’s rate integrity and contribution margin. - Ancillaries that matter

Wellness and medical-wellness sustain shoulder periods and broaden spend per guest. The EU wellness thesis continues to support ADR resilience through 2025. - Cost levers with proof

Labor productivity, energy efficiency, and procurement discipline. In a higher-for-longer cost regime, these are the guarantors of flow-through.

Risks to underwrite (so your IC doesn’t ask first)

ADR fragility in over-heated sub-markets. STR flagged softer months where tough comps and weather hit RevPAR—stress-test the plan for those windows.

Execution capacity. Brand conversion without on-property ops alignment won’t deliver ADR; pick partners with proven ramp-ups in that micro-market.

Debt and covenants. Positive RevPAR doesn’t immunize leverage—model refi at conservative rates and build covenant headroom (especially for MICE-heavy assets).

What this means if you’re buying or selling in 2025

For buyers: insist on a two-page NOI bridge (before any full data pack). If the bridge can’t be explained in plain language and basic math, move on.

For owners/sellers: you’ll maximize price by coming to market with a decision-ready playbook—operator short-list, phased CapEx, revenue roadmap, and a P&L that already reflects the first quick wins.

About Realivo (why partners call us first)

We combine brokerage with operating know-how. Our team curates one of Europe’s broadest hotel pipelines and pairs each opportunity with a practical value-creation plan—brand/operator fit, CapEx priorities, and revenue strategy—so investors see assets and answers in one place.

If you’re evaluating Europe in 2025, we’ll start with a short list that matches your thesis (market, key count, positioning) and a bridge from RevPAR to valuation that survives diligence.